A beginners guide for Financed Emissions

.png)

Financed Emissions

Financial institutions increasingly are starting to report on their climate related impact, like other organisations there are many reasons why now is the time to start (read more on this in our recent blog post).

In this post we will outline some of the key concepts as an introduction to Financed Emissions to build the foundations before we dive deeper in future posts.

What are Financed Emissions?

Financed emissions result from the investing or lending activities of an organisation. The idea is that if an organisation has funded a business or project, it is then responsible for a portion of those emissions based on its overall contribution to funding.

Why is measuring Financed Emissions so important?

Capital flows are crucial in the transition to Net Zero. If financial institutions transparently measure and report their financed emissions, stakeholders can make informed decisions about how they interact with these institutions.

Reporting of financed emissions has largely been a voluntary exercise so far. However, as reporting requirements become mandatory in some jurisdictions, investors and their portfolio companies will face increasing pressure to reduce emissions in line with the Paris Agreement (find out more in our overview on the reporting landscape here). This will likely drive change within the financial ecosystem and the broader business community that interacts with it.

The Climate Disclosure Project (CDP) found in a report published in 2020 that the portfolios of global financial institutions emit over 700x that the institutions direct emissions. So by far the biggest impact that financial institutions can have is working with their borrowers and portfolio companies to help them reduce the emissions of their activities.

How are they disclosed within an organisation's Greenhouse Gas Inventory?

Depending on the standard, financed emissions may have slightly different names. Under the GHG Protocol, financed emissions are called "Investments", while under the Partnership for Carbon Accounting Financials (PCAF) they are called "Financed Emissions", even though both terms refer to the same category of emissions.

Typically, financed emissions are reported under category 15 of Scope 3 in the GHG Protocol. However, this depends on how the organisation has set its organisational boundary in relation to its GHG inventory. If emissions associated with investments are included within either Scope 1 or 2, this is explicitly outlined in the inventory. For the most part, however, emissions from financed activities are disclosed under the downstream category of the protocol as noted below.

What is PCAF?

Although the GHG Protocol provides some guidance on calculating financed emissions, this area is specialised. To meet stakeholder requirements and promote comparability, the industry and the investment community began adopting the PCAF Standard.

PCAF originated in 2019, where banks, investors and fund managers came together from 5 different continents to create PCAF. This industry led initiative has rapidly expanded in the Americas, Europe, Africa and the Asia Pacific. The aim of PCAF was to standardise how financial institutions measure and disclose financed emissions and increase the number of financial institutions that commit to measuring and disclosing financed emissions.

PCAF developed the Global GHG Accounting and Reporting Standard for the Financial Industry (Financed Emissions Standard), with the methodologies used being approved by the GHG protocol in 2020. PCAF has also collaborated with the CDP, SBTi and the Task Force on Climate-related Financial Disclosures, indicating that this standard is trusted and utilised by industry professionals.

What is included in the Financed Emission Standard?

The Financed Emissions Standard addresses a major gap in the GHG Protocols' Scope 3 emissions framework, specifically Category 15 of "Investment Activities." For financial institutions, emissions associated with their investments account for the vast majority of emissions in their GHG inventory. Using the generic GHG calculations guidance from the GHG Protocol was simply not sufficient to meet the needs of both internal and external stakeholders or to drive emissions reduction actions.

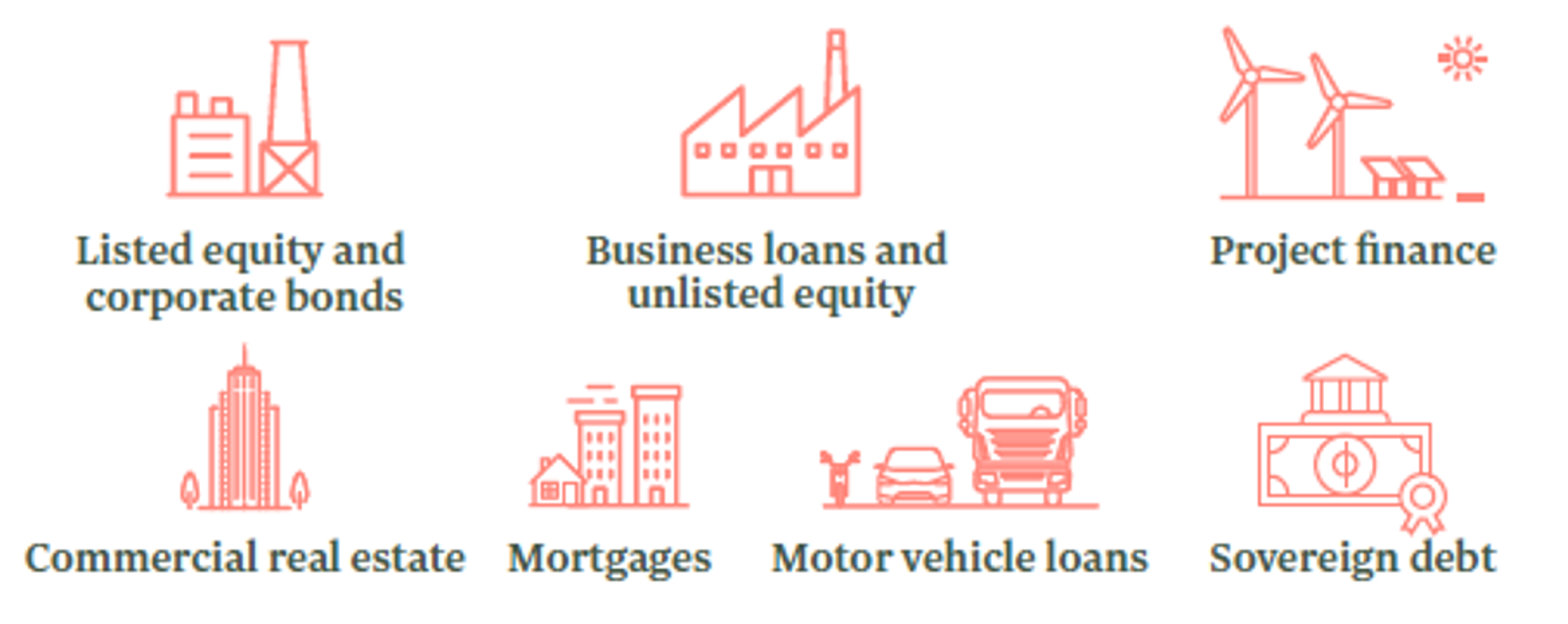

Through consultation with the industry, the Financed Emissions Standard developed specific methodologies associated with the various categories that form part of the portfolios of investors. These groups are known as asset classes under the standard and include the following:

A reference of where each of the asset class calculations methods can be found below:

- Listed Equity and Corporate Bonds (S5.1 pg 49)

- Business Loans and Unlisted Equity (S5.2 pg 66)

- Project Finance (S5.3 pg 79)

- Commercial Real Estate (S5.4 pg 88)

- Mortgages (S5.5 pg 94)

- Motor Vehicle Loans (S5.6 pg 101)

- Sovereign Debt (S5.7 pg 109)

Where to from here?

As carbon accounting is becoming a compliance requirement in countries around the world, Financial Institutions are generally amongst some of the first organisations who will be required to disclose their emissions.

Some financial institutions are already disclosing their financed emissions voluntarily, but the robustness and transparency required under the new standards may mean that sustainability and finance teams are going to be required to make some changes to their internal controls and data collection activities.

Sumday has developed a Financed Emissions course to upskill finance and sustainability teams on how to measure and report on financed emissions inline with the global standards. The course includes interactive materials and practical worked examples to help you apply the learnings in your organisation. Reach out for a chat with us or sign up for a free trial to get access to the course material today.